A pre-approval takes into consideration a client’s financial situation and creditworthiness to establish a maximum loan amount. An expedited pre-approval process is beneficial for lenders as it gives them a competitive edge in the market while also motivating prospective clients to take action and continue moving through their pipeline. This article explores ways to increase operational efficiency and ensure a smooth pre-approval process for both parties.

Key Takeaways

- Efficient processes enhance client experience and increase pre-approval success.

- Although the pre-approval process should be expedited, accuracy and compliance should be maintained.

- Expediting the pre-approval process may involve assessing your documentation-gathering strategies, communicating with underwriters, and implementing new technology.

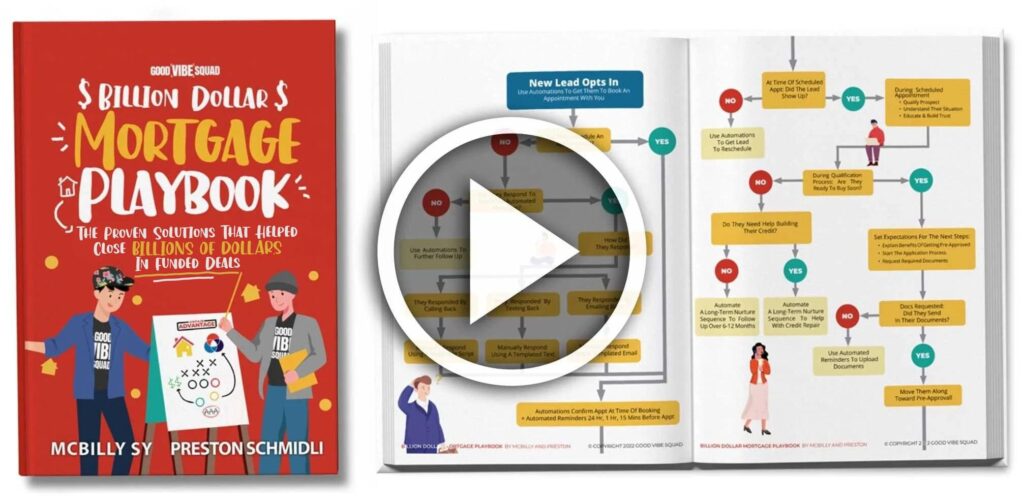

Get Our Billion Dollar Mortgage Playbook

Get the proven strategies that helped close Billions of dollars in funded deals!

Understanding the Components of the Pre-Approval Process

Pre-approval is a crucial step in major financial transactions like applying for a mortgage loan. Pre-approvals determine preliminary eligibility for a mortgage and typically consist of gathering documentation, credit checks, and financial health assessments.

Documentation:

During the pre-approval process for a loan or credit, clients must provide various documents to confirm their identity, financial status, and suitability to repay. The following are some of the most commonly requested documents:

- Identification:

Clients may need to provide a passport, driver’s license, or official document to verify their identity. - Proof of Income:

Providing pay stubs, tax returns, or any other documents showing consistent income can prove a client’s ability to repay any loan or credit line. - Employment Verification:

Clients may need to provide evidence of their past and sometimes current employment status. - Financial Statements:

Any other relevant financial records, such as bank and investment account statements, may be requested. - Debt Information:

Information about outstanding debts, including mortgages, credit card balances, and loans, may also be required. - Proof of Assets:

Evidence of valuable assets, such as real estate, vehicles, or precious possessions, may also need to be provided.

Credit Checks:

Lenders typically perform a credit check during the pre-approval process. This check provides insight into clients’ borrowing habits, payment history, and outstanding debts. A higher credit score generally indicates a more robust and dependable credit profile, which can lead to more favorable loan terms.

Financial Health Assessment:

Lenders evaluate client finances when they apply for a loan or credit to ensure they can repay it. This evaluation frequently contains:

- Debt-to-Income Ratio:

In general, a lower ratio is preferable because it shows the client has more income available to pay off new debt. - Income Stability:

Lenders will consider the consistency and steadiness of a client’s source of income. - Employment History:

A consistent work history may help with pre-approval. - Current Financial Commitments:

This includes any loans, credit card payments, and other financial obligations that clients currently have.

The pre-approval process may reveal eligibility and insights in terms of loan amount, interest rate, repayment period, etc. Remember that pre-approval is just an initial assessment based on the information a client provides; it’s not a guarantee for final approval. A client may also choose to work with a different lender, even after a pre-approval has been established. This is why it’s vital to start building rapport from the get-go to ensure a client is excited to work with you both now and in the future.

Tips to Speed Up Documentation Collection

Documentation is a key piece of the pre-approval process that can either aid in speeding the process up or act as a roadblock. Here are 11 ways to optimize your documentation collection process:

- Make use of digital platforms and technology:

Choose a user-friendly digital platform when requesting documents. Options include client portals, cloud storage like Google Drive or Dropbox, or other specialized software. Make sure whatever option you choose allows for easy and secure file uploads in various formats. - Make checklists:

Create a detailed checklist of required client documents organized by type (identification, financial, legal). Consider making these checklists available digitally for easy access. - Send electronic reminders:

Set up an automated alert system to notify clients of document due dates or missing items through email, SMS, or platform notifications. Schedule reminders at specific intervals to ensure smooth processing. - Provide learning resources:

Hold live educational sessions or webinars for clients on accurate documentation and digital tool benefits. Cover common mistakes people tend to make during the mortgage process and step-by-step instructions for moving through the pipeline to secure their dream home. - Provide personalized assistance:

Assign a dedicated client contact (perhaps a loan officer assistant) and offer live chat options or a helpline for immediate assistance during the loan process. - Prioritize a mobile-friendly process:

Choose a mobile-friendly platform or tool, as many clients will prefer to use their smartphones to submit documents. The convenience of mobile options often leads to higher action rates. - Gather regular feedback:

Get feedback from clients to learn how to improve your documentation collection process. - Consider gathering digital signatures:

Nowadays, certain platforms like DocuSign enable clients to sign contracts electronically, further speeding up the pre-approval and loan application process. Ensure you are following all local and federal compliance laws when utilizing such platforms. - Provide continual updates:

Update clients on document status, including received documents, pending documents, and required actions. - Protect data:

Ensure you are protecting client data at every step of the process, from the pre-approval all the way through the closed and funded loan. - Offer your words of appreciation:

Consider rewarding clients who submit documents on time with tokens of appreciation like personalized thank you cards.

Pre-Evaluating Client’s Credit Standing

It’s likely you’ll encounter several leads and prospects whose credit needs some work before they’ll be eligible to apply for a mortgage. Here is a list of the possible steps you could take in these situations:

- Provide Client Education Regarding Credit Reports:

You may consider creating PDF guides, blog posts, or videos explaining how to check a credit report and the different factors that go into assessing a credit profile. - Stress the Importance of Routine Checks:

Encourage individuals to check their credit reports regularly. They can obtain their free annual credit reports from Equifax, Experian, and TransUnion by visiting AnnualCreditReport.com. This is crucial for maintaining a healthy credit score and avoiding future financial problems. - Teach Clients How to Check for Mistakes:

Advise clients to review credit reports for errors like inaccurate account info, false reports of missed payments, or unrecognized accounts. Suggest they promptly report any discrepancies to the credit bureau for resolution. - Teach Clients How to Take Care of Potential Problems:

If your clients encounter any issues, guide them through the necessary steps to address and resolve them by filing disputes or creating an action plan to reduce the impact of legitimate negative entries. - Offer Strategies for Credit Improvement:

Provide clients with tips for gradually improving their credit scores, such as making timely payments, keeping their credit utilization below 30%, building a longer credit history, and cautioning against applying for too many new accounts at once. You may also refer them to a certified credit repair specialist. - Recommend Observation Services:

Provide information to customers about credit monitoring services so they can stay informed about changes to their credit reports. Numerous agencies provide alerts for brand-new accounts, balance changes, or possible identity theft these days which can help your clients stay proactive and protected. - Offer Long-Term Financial Planning:

Use this chance to talk to your clients about their long-term financial goals. Help them understand that having good credit is a crucial component of overall economic health and that prudent money management will enhance their credit standing. - Offer an Individualized Approach:

Keep in mind that every client’s situation is different. Adjust your advice to their unique situation and objectives. Others may aim for more excellent financial stability, while some may be working to build their credit in preparation for a significant purchase.

The Role of Technology in Expedited Pre-Approvals

Pre-approvals are one of the many processes that have been streamlined and expedited in the mortgage industry, largely thanks to technology. The pre-approval process is essential to buying a home because it gives prospective homeowners a clear understanding of their purchasing power and makes them stand out in competitive real estate markets. Technology has given loan officers to ability to automate certain tasks in addition to improving others. Here are some other ways technology can help:

- Automation of Tasks:

Pre-approvals have historically required intensive paperwork and manual data entry. A significant portion of this process can be automated by integrating technology. Nowadays, pre-approval letters can be issued with a click of a button. - Effective Data Collection:

Borrowers can electronically submit their financial information, such as income, employment history, credit scores, and debt obligations, using mortgage software solutions. Many software systems also offer valuable insights into Key Performance Indicators and other data points to consistently improve your offer and services. - Real-Time Verification:

Lenders can access real-time data to confirm the integrity of borrowers’ information. Automated verification expedites the verification process while lowering the risk of false information. - Credit and Risk Assessment:

Advanced algorithms can analyze financial data and credit reports to determine a candidate’s creditworthiness and risk profile. These algorithms consider several variables and offer a more precise and objective assessment of an applicant’s financial situation, lowering the possibility of bias and human error. - Predictive Analysis:

Technology enables lenders to use predictive analytics to determine borrowers’ default likelihood. Taking into account past data and trends aids lenders in making more informed decisions about pre-approvals. - Streamlined communication:

SMS and email tools offer accessible communication between borrowers, loan officers, underwriters, and other stakeholders. This eliminates the requirement for numerous back-and-forth communications via phone. - Enhanced Customer Experience:

Borrowers enjoy a more user-friendly pre-approval process with the implementation of mobile-friendly and digital solutions, making them more likely to recommend your services to others and utilize your services again in the future i.e., with refinancing.

Streamlined Pre-Approvals Make for a Better Experience for All

A streamlined pre-approval process improves functions, reduces errors, and saves time and money while optimizing resources, making it a win/win for both lenders and borrowers. This, in turn, builds stronger client relationships and establishes a reputation for you as the loan officer as being responsive and reliable. It’s a win/win for everyone involved in the mortgage process from beginning to end.

Meet the Most Comprehensive Digital Marketing Solution for Loan Officers

Unlimited leads? Check. Hybrid automations to cut follow-up times in half (or even better)? Double Check. Leads are great and all, but know what’s even better?

Gaining access to an award-winning system and proven process to actually convert them.

And EVEN BETTER than that?

A game plan for building strategic partnerships that put you in charge so you never have to rely on another professional for business again. See how we can help you maximize your time, income, freedom, and personal growth.