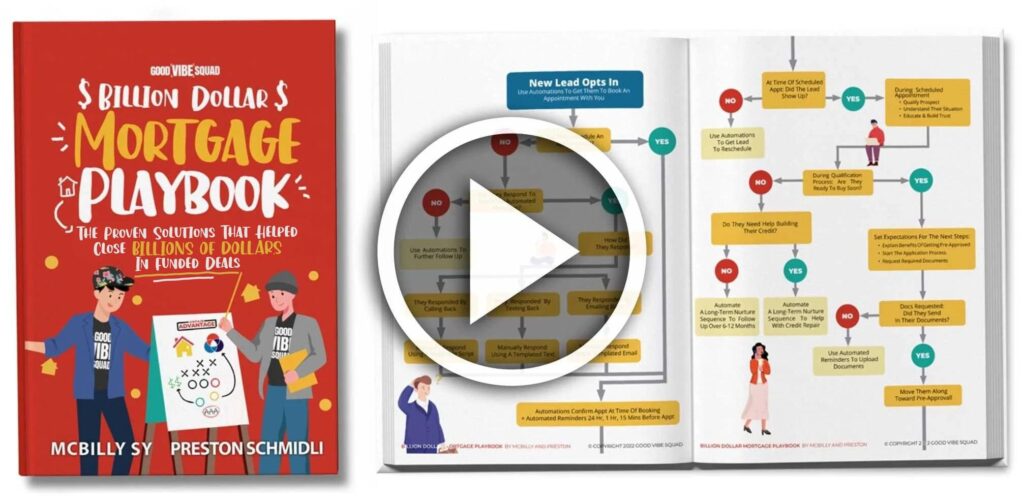

Mortgage Pipeline Bloat Comes in Many Forms

Mortgage pipeline bloat is a common issue that mortgage lenders face. It occurs when a lender has too many loans in their pipeline, which can lead to delays in processing and closing loans. This can be caused by a variety of factors, including a high volume of loan applications, inadequate staffing, and inefficient processes.

When a lender’s pipeline becomes bloated, it can cause a ripple effect throughout the entire organization, much like dominoes. Loan officers may become overwhelmed with the number of loans they are responsible for, which can lead to mistakes and delays. Underwriters may also struggle to keep up with the volume of loans they need to review, which can lead to longer processing times. And borrowers may become frustrated with the slow pace of the loan process, which can lead to lost business and a damaged reputation.

To prevent mortgage pipeline bloat, lenders need to take a proactive approach to managing their pipelines. This includes implementing efficient processes, hiring enough staff to handle the volume of loans, and regularly reviewing and optimizing their pipeline management strategies.

Other key strategies for preventing pipeline bloat include:

- Prioritizing loans based on their likelihood of closing.

- Implementing automated workflows and processes.

By focusing on loans that are most likely to close, lenders can reduce the number of loans in their pipeline and improve processing times. This can be done by using data analytics tools that identify trends in credit scores, debt-to-income ratios, and loan-to-value ratios.

Another strategy for preventing pipeline bloat is to implement automated workflows and processes. This can help streamline the loan process and reduce the amount of time and resources required to process each loan. By automating tasks such as document collection, underwriting, and loan closing, lenders can reduce the risk of delays and errors while improving overall efficiency.